Doubling up: why materiality matters and double materiality is the essential next step

Materiality is a key principle used to determine what ESG (environmental, social and governance) considerations really mean to organisations and how they align with your business strategy. In this blog, Ricardo's ESG experts, guide us through the theory and practicalities of materiality and explain the importance of the shift towards the newer more holistic concept of double materiality.

What is materiality?

Assessing materiality is the process of determining which issues or topics are important to a business. A materiality assessment is key for organisations wanting to transparently show their commitment to improving their ESG criteria. The outcomes inform business planning, highlighting risks to address as well as opportunities to explore.

An organisation’s materiality is often evaluated at the sector level by third party ESG assessment providers to allow potential investors to understand the full breadth of ESG risks and opportunities associated with that organisation. Understanding your organisation’s material issues can help you to mitigate risks and exploit opportunities, thus making your organisation more attractive to potential investors and customers.

There are two commonly used types of materiality – financial materiality and impact materiality. When used individually, these can be referred to as a single materiality assessment.

Financial materiality looks inward at the planet and society’s impact on business operations. This concept has traditionally formed the basis of materiality assessments in annual reports, aimed at identifying an organisation’s ESG-related risks and opportunities. Domestic and international standards that look at financial materiality include the International Sustainability Standards Board (ISSB), the Sustainability Accounting Standards Board (SASB), the International Financial Reporting Standards (IFRS) and the Task Force for Climate-Related Financial Disclosures (TCFD).

Impact materiality looks outward at a business’s impact on the planet and society. Impact materiality is usually associated with sustainability as it allows an organisation to understand how it can have a more positive impact on the world around it. Organisations that perform a single materiality assessment as a basis for an sustainability strategy will typically opt for impact materiality rather than financial. The Global Reporting Initiative (GRI) is an international standards framework based on impact materiality.

Impact materiality

Your business's outward impact on the planet and society

Financial materiality

The planet and society's impact on your business

If, for example, an organisation was looking at the topic of climate change from an impact materiality lens, it might consider the emissions the company emits. If it was considering the topic from a financial lens, however, it might look at the profit implications of disruptions to the supply chain due to severe weather events.

What is double materiality?

Double materiality is a relatively new concept in the world of ESG reporting and strategy. The concept combines impact materiality with financial materiality. By considering issues from more than one angle, an organisation has more holistic view of the risks and opportunities it faces.

By assessing a business from this viewpoint, a company can best determine in which areas it might have the biggest impacts (e.g., employing people from local communities and thus helping the economic outlook of a particular region) and which areas it has the most need to seize opportunities or mitigate risks that may impact the organisation financially (e.g., avoiding environmental fines by limiting pollution from company activities). The findings of a double materiality assessment can enable organisations to build even more robust and resilient business strategies that satisfy the demands of all stakeholders.

Internationally, leading companies reporting on material issues are moving towards a double materiality framework.

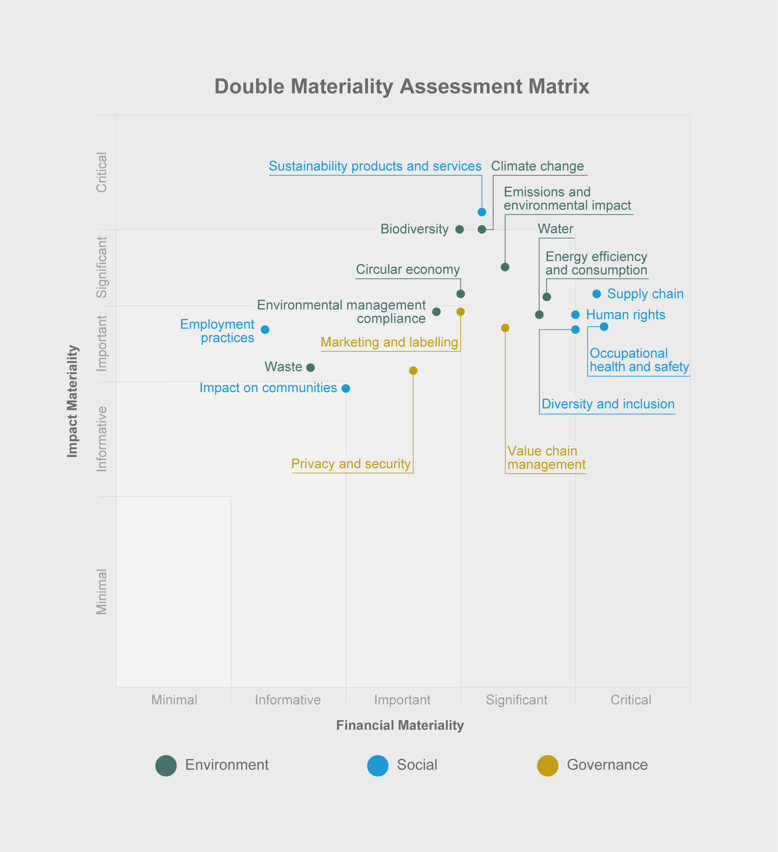

Example of a double materiality matrix

Legislation for double materiality reporting

Legislators are moving to increase transparency when it comes to sustainability efforts so, although double materiality is not yet standard best practice in the world of ESG reporting, the reporting landscape and regulations are headed in that direction.

Double materiality was first defined by the European Commission and accepted as part of the Non-Financial Reporting Directive (NFRD) in 2019. More recently, in November 2022, the European Parliament adopted the Corporate Sustainability Reporting Directive (CSRD). The CSRD will be phased into practice starting in 2025 (based on an organisation’s financial year starting in 2024).

Reporting under the CSRD mandates that organisations take a double materiality approach. The directive “require [s] [businesses] to report both on the impacts of the activities of the [business] on people and the environment, and on how sustainability matters affect the [business] ”. Depending on the outcomes of its double materiality assessment, an organisation might be required to report on topical European Sustainability Reporting Standards (ESRSs).

Required compliance with the CSRD is dependent on the size of an organisation and how it is required to report in the EU. The CSRD covers many more businesses than the current NFRD – it is likely that 50,000 European organisations and 10,000 foreign companies will be within the scope of the CSRD.

Do check if your business will be included within scope of the CSRD and, if it is, when you will be required to start reporting. Accountancy Europe has compiled a helpful breakdown of which types of companies will have to comply and when.

To support the implementation of the CSRD, the European Financial Reporting Advisory Group (EFRAG) prepared sector-agnostic ESRSs. Standards were finalised in November 2022. Another EFRAG draft, published in January 2022, provides guidelines on how to successfully complete a double materiality assessment. It is important to note that these conceptual guidelines are still in draft form so there is no officially defined approach to double materiality at this time. Nonetheless, guidelines such as these are very helpful as companies begin to navigate the landscape of double materiality and CSRD compliance.

Putting these recommendations into practice, however, can be a daunting task for organisations. Ricardo can help with both conducting a robust double materiality assessment and reporting the findings in line with the relevant legislation for your organisation.

Why you should start your double materiality assessment now

Completing a double materiality assessment sooner rather than later will allow your organisation to determine which topics it should be reporting on and will inform its business and sustainability strategies. Double materiality assessments can take several months, depending on the size and scope of the organisation.

If you already fall under the existing NFRD, you will need to report under the CSRD as soon as 2025 (based on FY24). Starting the assessment process as early as possible will allow your organisation to analyse, interpret and begin to act on your materiality results well in advance of the annual reporting cycle. Integrating these results into strategy decisions, transition plans and key performance indicators shows stakeholders that your company is serious about compliance, sustainability and staying ahead of the curve.

How to get started with a double materiality assessment

- Determine if your organisation has already completed any impact or financial materiality assessments. These can be an excellent jumping off point for this next iteration of materiality.

- Even if you have completed a materiality assessment before, it is crucial to make sure your organisation has an up-to-date list of stakeholders across a wide range of areas. Engaging with these stakeholders is imperative to the materiality process.

- Analyse EFRAG’s Double Materiality draft conceptual guidelines and think about how they would work in practice for your organisation.

Double materiality is complex but, when done right, can place your organisation in a strong position to improve its strategy, maintain compliance with recognised standards and tackle its ESG goals and aspirations head on.

Ricardo’s experts are here to guide you no matter what stage you are at on your ESG and sustainability journey. Please get in touch with any questions and to find out more about how we can help you to determine the most effective pathway to your ESG and sustainability goals and how we can support you with implementing the actions required for success.